The 3-Week Loan: How AI Cuts Underwriting from Days to Minutes

This blog explores how AI is transforming the lending industry by slashing underwriting times from weeks to minutes. By automating manual document reviews and ratio calculations, financial institutions can provide instant decisions while actually improving risk accuracy. The piece highlights how this shift not only boosts bank profitability and volume but also creates a dramatically better experience for the modern borrower.

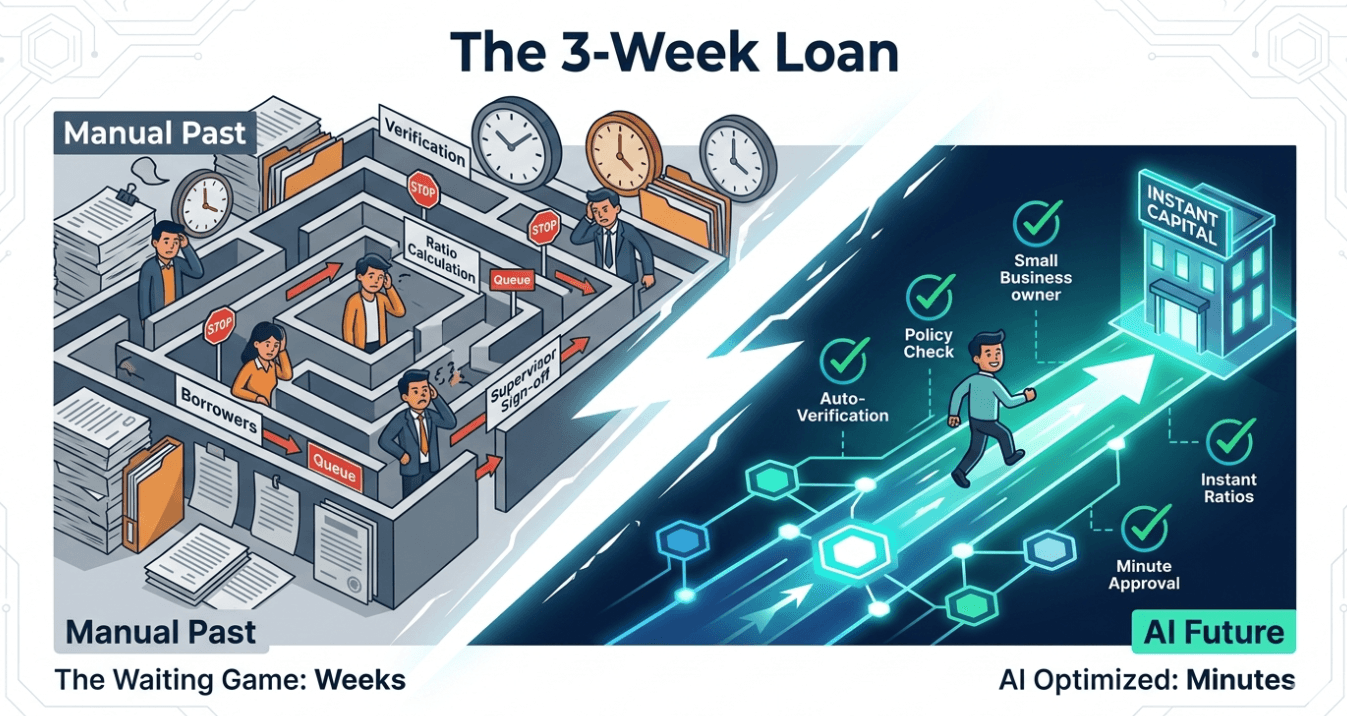

The waiting game that costs billions

A small business owner applies for a loan. She needs capital to buy inventory for the peak season. The bank takes her application. She waits one week. The bank requests additional documents. She provides them. She waits another week. The bank asks clarifying questions. She answers. She waits another week. Finally, three weeks after applying, the bank approves the loan. The peak season has started. The inventory arrives late. The opportunity is lost.

This story repeats millions of times annually. The average commercial loan takes two to three weeks to underwrite. The average consumer loan takes three to five days. The wait is not due to lazy bankers. It is due to manual processes. Humans review documents. Humans calculate ratios. Humans verify income. Humans check collateral. Each human touchpoint adds hours or days. Each handoff adds delay. AI in financial services eliminates the humans from routine underwriting decisions. The result is approvals in minutes, not weeks. The customer gets capital when they need it. The bank originates more loans with the same staff.

The anatomy of a manual underwriting process

A traditional loan underwriting process involves seven distinct steps. First, the customer submits an application with supporting documents. Second, a loan officer reviews the application for completeness. Third, the application is assigned to an underwriter. Fourth, the underwriter verifies income and employment using bank statements and tax returns. Fifth, the underwriter calculates debt-to-income and loan-to-value ratios. Sixth, the underwriter checks credit reports and public records. Seventh, a senior underwriter approves or declines the decision.

Every one of these steps is manual. Every step introduces delay. Every handoff between steps adds waiting time. A loan that requires thirty minutes of actual work takes three weeks to complete because the work is not continuous. The loan sits in queues. The loan waits for the next available reviewer. The loan waits for document clarification. The loan waits for supervisor sign-off. AI collapses these seven steps into one continuous process that completes in minutes.

How AI underwriting actually works

AI in financial services replaces manual review with automated decisioning. The borrower submits an application through a digital portal. The AI immediately extracts data from the application. It pulls credit reports from bureaus. It accesses income and employment data through connected payroll systems. It verifies assets by connecting to bank accounts with customer permission. It checks public records for liens or bankruptcies. All of this happens in seconds, not days.

The AI then applies the lender's credit policy. Debt-to-income below forty-three percent. Loan-to-value below eighty percent. Minimum credit score six hundred eighty. These rules are the same as a human underwriter would use. The AI simply applies them faster and more consistently. A human underwriter might miss a calculation error or overlook a document discrepancy at 4 PM on a Friday. The AI never gets tired. It applies the same scrutiny to the first loan of the day and the thousandth.

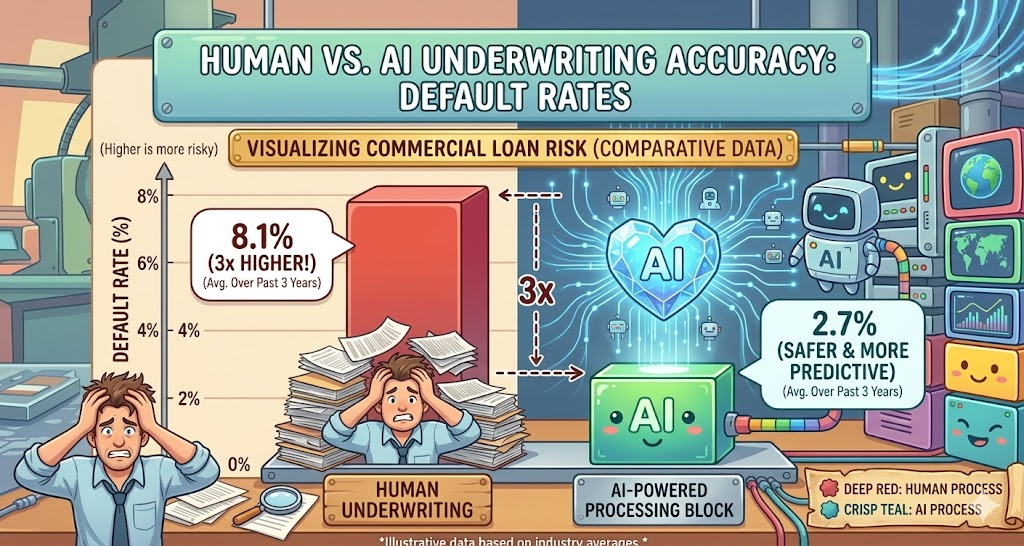

The risk paradox

Lenders worry that automated underwriting increases risk. The opposite is true. AI in financial services reduces risk by applying policy consistently and by detecting patterns that humans miss. A human underwriter might approve a loan that technically meets guidelines but has subtle risk indicators. The borrower has a history of late payments on a specific type of debt. The borrower's income is stable but from an industry facing decline. The AI learns to weight these subtle signals.

One community bank deployed AI underwriting for small business loans. They ran the AI alongside their human underwriters for six months. The AI approved loans that humans had declined. Those loans performed well. The AI declined loans that humans had approved. Those loans defaulted at three times the rate of AI-approved loans. The AI was not more strict. It was more accurate. It saw patterns that human underwriters missed because the humans were overwhelmed with volume.

The borrower experience transformation

The borrower experience under AI underwriting is dramatically better. The customer applies online in ten minutes. They connect their bank account securely. They authorize payroll data access. They submit tax returns electronically. Fifteen minutes after hitting submit, they receive a decision. Approved. Conditional approval pending verification. Declined with explanation.

One online lender used AI underwriting to reduce average approval time from four days to eighteen minutes. Customer satisfaction scores for the lending process increased by fifty-two points. The most common customer comment was not about the interest rate or the loan terms. It was "I cannot believe how fast this was." Speed became their competitive advantage. Borrowers who needed capital quickly chose them over banks that took weeks. The lender grew loan volume by three hundred percent in two years without increasing underwriting headcount.

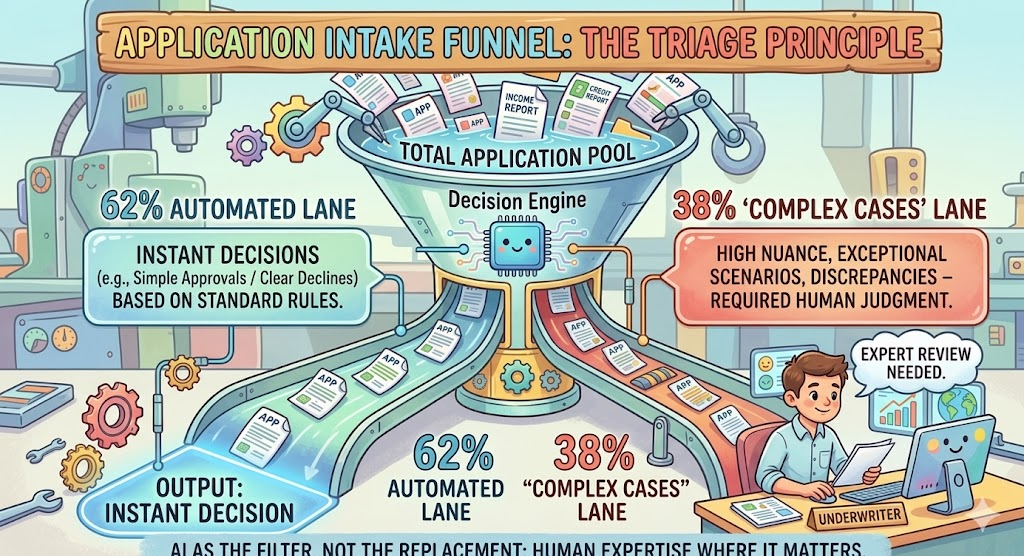

The exception handling problem

Not every loan can be auto-approved. Complex situations require human judgment. A borrower with self-employment income and multiple real estate holdings. A borrower with recent divorce affecting credit. A borrower with foreign assets. AI in financial services handles exceptions by flagging them for human review.

The AI processes the straightforward loans automatically. The underwriter receives only the complex cases. This triage increases underwriter productivity because they spend time only where judgment adds value. One mortgage lender implemented AI triage and found that sixty-two percent of loan applications could be auto-approved or auto-declined. Human underwriters focused on the remaining thirty-eight percent. The underwriters closed four times as many loans per week because they stopped touching every file. The auto-decisions were more consistent than manual decisions and had lower default rates.

Real results from a regional bank

A regional bank with twelve billion dollars in assets processed consumer loan applications manually. Application to decision averaged nine days. The bank employed fifteen underwriters. Loan volume was growing slowly because the underwriting process was a bottleneck.

The bank deployed AI automated underwriting integrated with their loan origination system. They started with small personal loans under twenty thousand dollars. The AI received all applications. It pulled credit, verified income, checked internal fraud databases, and applied bank policy. Approved loans moved directly to funding. Declined loans received explanation letters automatically. Exception loans routed to human underwriters.

Within ninety days, average approval time dropped from nine days to twenty-two minutes. The bank increased loan volume by forty-one percent without adding underwriters. Fourteen of the fifteen underwriters were reassigned to exception handling, quality assurance, and complex loan analysis. The bank saved an estimated four hundred thousand dollars annually in underwriting labor while originating significantly more loans. Default rates on AI-approved loans were eleven percent lower than on previously manually-approved loans.

The fair lending question

Regulators require fair lending. No discrimination based on race, gender, age, or other protected characteristics. AI in financial services raises valid concerns. An AI model trained on historical data might learn historical discrimination. If past underwriters approved fewer loans to minority applicants, the AI might learn that pattern.

This risk is real and manageable. Responsible AI underwriting includes fairness testing. The lender tests model outcomes across protected classes before deployment. Disparate impact triggers model adjustment. The model is retrained on data that excludes prohibited variables. The lender documents all testing and adjustments for regulators.

The counterintuitive truth is that AI can be more fair than humans. Human underwriters have unconscious biases that they cannot articulate or control. AI bias is measurable and correctable. A bank that deploys AI underwriting with proper fairness testing can demonstrate to regulators exactly how decisions are made. No human underwriter can provide that transparency.

The thin-file opportunity

Millions of Americans have thin credit files. They have no credit cards. They have no installment loans. They pay rent, utilities, and phone bills in cash or through bank accounts that do not report to credit bureaus. Traditional underwriting cannot score these borrowers. They are invisible.

AI in financial services scores thin-file borrowers using alternative data. Rent payment history. Utility payment history. Bank account cash flow patterns. Even mobile phone bill payment history. The AI finds patterns in this data that predict creditworthiness. A borrower who pays rent on time for two years is low risk regardless of their credit file. A borrower with consistent bank account balances and no overdrafts is low risk.

One fintech lender used AI alternative data scoring to approve loans for seventy percent of thin-file applicants that traditional models would have declined. Default rates on these loans were only slightly higher than on traditional borrowers. The lender captured an entirely new market segment that competitors ignored. The borrowers were grateful for the opportunity to build credit history.

The integration path for lending leaders

Your first step is selecting a decision domain. Do not automate all loan types simultaneously. Choose one product with clear policy rules and sufficient historical volume. Personal loans under a certain size. Small business loans. Credit card applications. Start narrow.

Your second step is data preparation. Your AI model needs historical loan applications with known outcomes. Approved loans that repaid. Approved loans that defaulted. Declined loans that would have defaulted had they been approved. You need at least ten thousand completed applications for a reliable model. Smaller portfolios can use industry benchmark models or start with rules-based automation that learns over time.

Your third step is model development. Your data science team or vendor builds a model predicting default probability for each applicant. The model is trained on historical data and tested on holdout data. Validation confirms that the model outperforms your current underwriting process.

Your fourth step is pilot deployment. Run the AI alongside your human underwriters for sixty to ninety days. Compare decisions. Compare outcomes. Refine the model based on pilot results. After validation, switch to active decisioning for your selected product. The entire process from planning to active deployment typically takes four to six months for a first use case. Subsequent products deploy faster as infrastructure and expertise accumulate.

Conclusion

The three-week loan is not a necessity. It is a choice. A choice to underwrite manually. A choice to make customers wait. A choice to lose business to faster competitors. AI in financial services removes the choice. Automated underwriting approves loans in minutes. It applies policy consistently. It detects subtle risk patterns. It frees human underwriters for complex cases. The technology is proven. The ROI is measurable. The customer experience is dramatically better. The only question is whether your institution will lead or follow.

Related Blogs

View All

How AI Pricing Fills Empty Hotel Rooms and Maximizes Revenue

Recent

The Machine Failure: How AI Predicts Breakdowns Before They Stop Production

Recent

The Route That Bleeds Cash: How AI Cuts Fuel Costs Without Reducing Deliveries

Recent

The Support Crisis: How AI in Ecommerce Cuts Costs and Delights Customers at Scale

Recent