The Silent Exit: How AI Predicts Which Customers Will Leave Next Week

This blog examines how AI allows banks to move from reactive churn reporting to predictive customer retention. It details how machine learning identifies the "silent exit"—the subtle behavioural shifts that signal a customer is about to leave long before they actually close their account.

The quietest loss in banking

A customer closes their account. No drama. No complaint. No angry phone call. They simply move their direct deposits to another bank. They transfer their savings. They cancel their credit card. The relationship ends. The bank never saw it coming. The customer was profitable for years. Acquisition cost was high. Lifetime value was never realized. Now they are gone.

This is the silent exit. It happens millions of times annually. Most banks discover churn after it happens. A report arrives at the end of the month showing net account losses. The marketing team reviews the numbers. They shrug. Churn is expected. Customers leave. New customers arrive. The cycle continues. But not all churn is inevitable. Much of it is predictable. AI in financial services predicts which customers are planning to leave before they actually leave. The bank intervenes. The customer stays. The relationship continues.

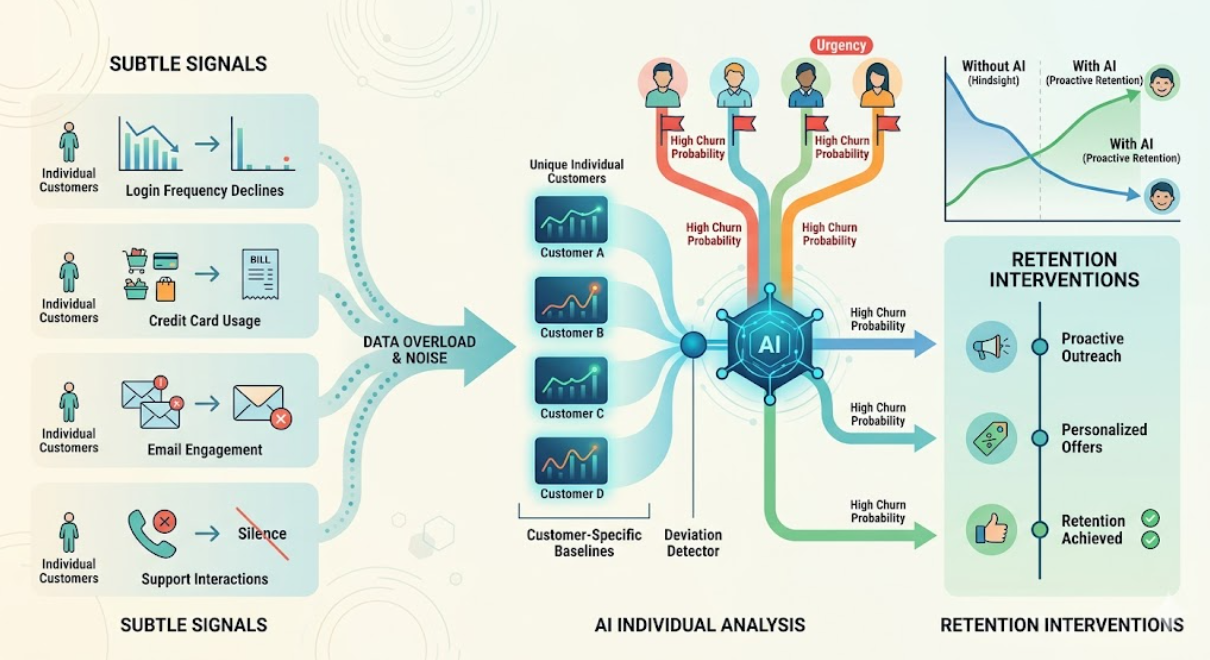

The anatomy of silent exit

Customers rarely leave without warning. They send signals weeks or months before closing the account. The signals are subtle. A customer who previously logged in daily now logs in weekly. A customer who used their credit card for all purchases now uses it only for recurring bills. A customer who responded to emails now ignores them. A customer who called support occasionally suddenly stops calling. Each signal alone is noise. Together, they form a pattern.

Traditional churn analysis looks at aggregate data. Average login frequency declined. Average transaction volume decreased. This tells the bank that churn is happening. It does not tell the bank which customers are at risk. AI in financial services analyses individual behaviour patterns. The model learns what normal looks like for each customer. When behaviour deviates from normal, the AI calculates a churn probability score. Customers above a threshold receive retention interventions before they leave.

The signals that predict departure

AI in financial services analyses dozens of signals to predict churn. Login frequency changes. A customer who logged in fifteen times per month dropping to five times per month is a signal. Transaction volume changes. A customer reducing credit card spend by sixty percent over eight weeks is a signal. Product mix changes. A customer who closes a savings account but keeps checking is a signal. Support interaction changes. A customer who had a negative support interaction and then goes silent is a strong signal.

The most powerful signal is rarely measured. Customer effort score. How much work did the customer need to do to accomplish their goal? A customer who called support three times to resolve a single issue is high effort. That customer is likely to leave within ninety days. The AI learns the relationship between effort and churn. It flags high-effort customers for proactive outreach, not to apologize, but to fix the underlying process.

One regional bank analysed two years of customer behaviour data and identified thirty-seven distinct churn signals. The most predictive was a combination of reduced digital engagement and increased support calls. Customers showing both signals had a sixty-eight percent probability of closing their accounts within sixty days. The bank had never connected these dots because the data lived in different systems.

The timing problem

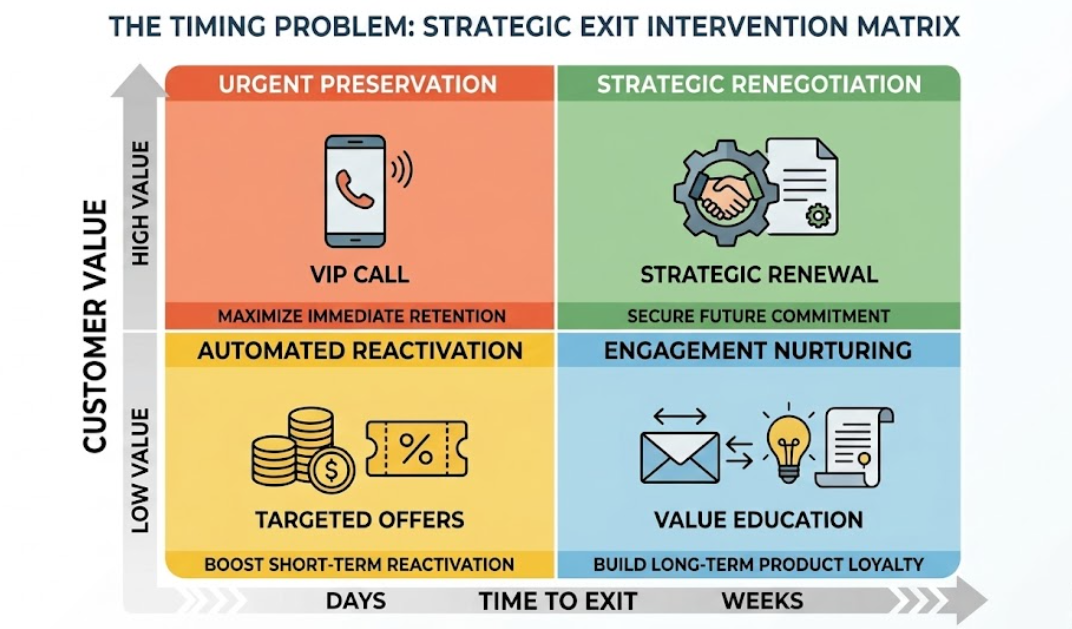

Knowing a customer is at risk is useful. Knowing when they will leave is better. AI in financial services predicts not just probability but timing. A customer with a churn probability of eighty percent is very likely to leave. But will they leave next week, next month, or next quarter? The answer determines the intervention strategy.

Customers predicted to leave soon need immediate, high-touch interventions. A phone call from a relationship manager. A personalized retention offer. A service recovery gesture. Customers predicted to leave later can receive automated, lower-cost interventions. Personalized email campaigns. Digital offers. Product recommendations. The AI optimizes the timing and channel of each intervention.

The proactive retention call

The best time to retain a customer is before they decide to leave. Once a customer has decided, retention becomes difficult and expensive. They have already mentally left. They have opened an account elsewhere. Reversing that decision requires significant incentive. AI calls allow banks to intervene at the moment of indecision, before the customer commits to leaving.

A large credit union implemented AI churn prediction and proactive retention calling. The model identified customers with churn probability above seventy percent. These customers received a call within forty-eight hours from a retention specialist. The specialist did not offer a generic discount. They reviewed the customer's specific situation using AI-generated insights. "We noticed you stopped using your mobile banking app. Is there something we can help with?" The conversation was personal and relevant.

The credit union achieved a thirty-eight percent reduction in churn among contacted customers. The cost of the retention program was far lower than the cost of acquiring new customers to replace those lost. The credit union calculated that every dollar spent on proactive retention generated seven dollars in retained lifetime value

.

The root cause analysis

Churn prediction is valuable. Churn prevention is more valuable. Preventing churn requires understanding why customers leave. AI in financial services identifies root causes by analysing patterns across thousands of churned customers. Are customers leaving due to service issues? Pricing? Product gaps? Competitor offers?

One bank discovered through AI analysis that customers who opened a checking account and did not add a savings account within ninety days were three times more likely to churn in the first year. They were not fully engaged. They had not consolidated their banking. They maintained other relationships elsewhere. The bank launched a targeted campaign offering a savings account bonus to new checking customers at day sixty. Attachment rates increased by twenty-four percent. First-year churn dropped by eighteen percent.

Another bank discovered that customers who switched from premium to basic checking were signalling future churn. Sixty percent of these customers closed all accounts within six months. The bank created a retention workflow for downgrading customers. When a customer initiated a downgrade, the system automatically offered a retention specialist call. The specialist uncovered the real reason. Often it was a temporary financial constraint or a misunderstanding of fees. Half of the customers accepted an offer to stay in premium with adjusted terms.

The win-back opportunity

Customers who leave are not gone forever. Some return. The key is timing and offer. Contact a former customer too soon and they are still angry. Contact them too late and they have fully adopted the competitor. AI in financial services identifies the optimal win-back window for each customer segment.

A national bank analysed win-back campaigns across one hundred thousand former customers. The AI found that customers who left due to service issues were most receptive to win-back offers at ninety to one hundred twenty days after departure. Customers who left due to price were most receptive at thirty to sixty days. Customers who left because they moved out of the bank's geographic footprint never returned regardless of offer.

The bank restructured their win-back program based on these insights. Campaign response rates increased by forty-two percent. Cost per recovered customer dropped by thirty-five percent. The bank recovered over fifteen thousand former customers in the first year of AI-guided win-back.

The cross-sell that prevents churn

The strongest predictor of customer retention is product depth. A customer with one product has high churn risk. A customer with two products has lower risk. A customer with three or more products has very low churn risk. Each additional product creates switching costs. The customer has more accounts to move, more automatic payments to update, more relationships to sever.

AI in financial services predicts which customers are ready for which products. The model analyses transaction data, life events, and behavioural signals. A customer who recently received a large deposit may need a savings account or investment product. A customer who frequently books travel may need a rewards credit card. A customer whose pay check grew significantly may need premium checking.

One online bank used AI cross-sell recommendations to increase product depth. The AI presented offers to customers through digital channels at the moment of highest relevance. A customer checking their balance saw an offer for a savings account. A customer paying bills saw an offer for an overdraft protection line. The conversion rate on AI-timed offers was three times higher than on batch email campaigns. Product depth increased by twenty-two percent. Churn among customers who accepted a cross-sell offer was seventy percent lower than among customers who did not.

The life event opportunity

Customers are most likely to churn during major life events. Moving to a new city. Getting married. Having a child. Changing jobs. Retiring. During these transitions, customers reevaluate all their financial relationships. They are open to switching. They are also open to deepening their relationship if the bank shows up at the right moment.

AI in financial services detects life events through transaction data. A large payment to a moving company suggests relocation. A jewellery store purchase suggests engagement or wedding. A paediatrician payment suggests a new baby. A retirement plan distribution suggests retirement. The AI flags these signals and triggers personalized outreach.

A community bank implemented life event detection and triggered relationship manager calls for high-value customers showing life event signals. The manager did not sell. They offered congratulations and asked if there was anything the bank could do to help with the transition. The calls generated goodwill. They also generated new business. Customers who received a life event call opened an average of one point seven new products within ninety days. Churn among called customers was sixty-three percent lower than among the control group.

The implementation path for retention leaders

Your first step is data consolidation. You need customer transaction history, digital engagement logs, support interaction records, and account status changes. The data may live in your core banking system, CRM, support platform, and digital analytics tools. Consolidate it into a single customer view.

Your second step is defining churn. For deposit accounts, churn is account closure. For credit cards, churn is zero activity for six consecutive months. For loans, churn is payoff without new origination. Choose definitions that match your business model.

Your third step is model development. Your data science team or vendor builds a model predicting churn probability over a defined time horizon. Sixty days. Ninety days. The model is trained on historical data where you know which customers churned and which stayed.

Your fourth step is intervention design. Define what happens when a customer receives a high churn score. Automated email? Retention call? Special offer? The intervention should match the predicted churn reason. Service issue customers need service recovery. Price sensitive customers need offers. Disengaged customers need education.

Your fifth step is deployment and measurement. Run the model weekly to generate churn scores. Trigger interventions for high-score customers. Measure churn rates among intervened customers compared to a control group receiving no intervention. The difference is your retention lift. The full program typically takes four to six months from planning to active deployment. The reduction in churn is visible within sixty days of deployment.

Conclusion

The silent exit is not inevitable. Customers send signals weeks before leaving. Login frequency drops. Transaction volume declines. Support interactions change. These signals are invisible to aggregate reports. They are obvious to AI. Predictive models identify at-risk customers before they decide to leave. Proactive retention interventions convert many of these customers from leavers to stayers. The investment in AI churn prediction pays for itself many times over in retained customer lifetime value. The question is not whether your customers are planning to leave. Some are. The question is whether you will know who they are before they go.

Related Blogs

View All

How AI Pricing Fills Empty Hotel Rooms and Maximizes Revenue

Recent

The Machine Failure: How AI Predicts Breakdowns Before They Stop Production

Recent

The Route That Bleeds Cash: How AI Cuts Fuel Costs Without Reducing Deliveries

Recent

The Support Crisis: How AI in Ecommerce Cuts Costs and Delights Customers at Scale

Recent